The financial world is officially split into three distinct systems. Which one will eventually hold your assets? Figuring out exactly where capital is moving right now isn’t easy. The battle lines are clearly drawn between traditional banking, crypto-native companies and decentralized protocols. If you’ve spent any time researching the space; you know the defi vs tradfi debate gets intense pretty fast.

And if you are wondering how, you specifically fit into the broader TradFi, CeFi and DeFi landscape, you aren’t the only one. In this guide, we’ll break down how these three ecosystems actually work beneath the surface, where their real failure points lie, and which system probably makes the most sense for your portfolio today.

What Is TradFi (Traditional Finance)?

Traditional finance or TradFi is the system most people already use every day. It includes central banks, commercial banks, stock exchanges, payment networks and insurance companies. Think of institutions like JPMorgan Chase, Goldman Sachs and infrastructure like SWIFT or NASDAQ.

At its core, TradFi runs on fiat money and private ledgers meaning transactions are recorded and controlled by institutions not visible to the public. To participate, you must go through identity checks (KYC) and the entire system is governed by regulators like the Federal Reserve.

One key concept here is fractional reserve banking; banks don’t keep all your deposited money in a vault. They lend out a large portion of it to generate profit, effectively creating more money in the system than they physically hold.

In simple terms, TradFi works because you trust institutions to manage, store and move your money on your behalf.

What Are the Pros and Cons of Traditional Finance?

Traditional finance has been around forever and keeps the world moving but it’s far from perfect.

Pros

- Security: Big banks like JPMorgan Chase strict rules so your money is generally safe.

- Accessibility: Most people can open a bank account, get a card or take a loan somewhere near them.

- Consumer Protection: Regulators like the Federal Reserve step in to prevent the worst mistakes.

- Transaction Speed (for local payments): Paying with Visa Inc. or Mastercard is almost instant but only locally.

Cons

- High Fees and Costs: Sending money through the SWIFT or using other banking services can get expensive fast.

- Slow and Inefficient Processes: International transfers and settlements often take several days to complete.

- Limited Access and Flexibility: Millions even billions of people remain unbanked or face strict barrier to open an account.

What is CeFi (Centralized Finance)?

Centralized finance (CeFi) sits right between traditional banking and crypto. It is made up of companies that offers crypto service but operate like regulated businesses with user accounts, customer support and compliance teams. Platforms like Binance, Kraken, Crypto.com and Nexo are typical examples. The key thing to understand, CeFi is custodial. That means the platform holds your private keys not you.

Trades don’t happen on a public blockchain. Instead, they’re processed off chain on the company’s internal database. That’s why transactions are fast, cheap (often zero gas fees) and can scale to thousands per second. But there is a catch; you don’t fully own your crypto until you withdraw it to your own wallet. So, while CeFi feels like crypto; it still relies on trust just like traditional finance only with different players.

What Are the Pros and Cons of CeFi?

CeFi makes crypto easier to use but it comes with trade-offs.

Pros

- User Friendly Experience: Platforms like Coinbase and Binance make buying, trading and earning crypto almost as simple as using a regular shopping app.

- Enhanced Security and Compliance: These companies follow regulations and offers protections like two factor authentication and insurance on some assets.

- Speed and Flexibility: Off-chain trading allows thousands of transactions per second without waiting for blockchain confirmations.

Cons

- Custody and Counterparty Risks: Your funds are controlled by the platform, if it fails or get hacked (like FTX in 2022) you could lose everything.

- Higher Fees and Costs: Some platforms charge trading fees, withdrawal fees and management fees.

- Limited Transparency: Everything happens on internal ledgers, so you have to trust the company’s reporting and honesty.

What Is DeFi (Decentralized Finance)?

DeFi is basically finance without the middlemen. Instead of banks or companies, it runs entirely on public blockchains like Ethereum, Solana and Avalanche using smart contracts self-executing code that handles transactions automatically.

Anyone with a crypto wallet can jump in anytime, anywhere; with no credit checks or KYC. Governance usually happens through DAOs (Decentralized Autonomous Organizations) letting token holder vote on key protocol decisions.

That said not everything is fully decentralized. For instance, Uniswap Labs still guide the interface and development roadmap even though it doesn’t control the underlying smart contracts. In short DeFi moves trust from people and institutions to code giving users more control but also more responsibility.

What Are the Pros and Cons of Decentralized Finance?

DeFi opens new possibilities but it’s not without risks.

Pros

- Accessibility and Inclusion: Anyone with a wallet can participate, no bank account needed.

- Cost Efficiency: No middlemen so fees are often lower than TradFi or CeFi.

- Transparency and Security: All transactions are on-chain and auditable.

- Innovation Features: Yield farming, liquidity pools and algorithmic trading aren’t possible in traditional systems.

Cons

- Smart Contract Vulnerabilities: Bugs or exploits in the code can drain funds instantly leaving users helpless.

- No Consumer Protections: There’s no insurance or recourse if something goes wrong so mistakes can be costly.

- Volatility and Liquidity Risks: Prices of assets can swing wildly, and low liquidity can make losses even bigger.

- User Error: Losing private keys or sending funds to the wrong address is permanent and can wipe out holdings.

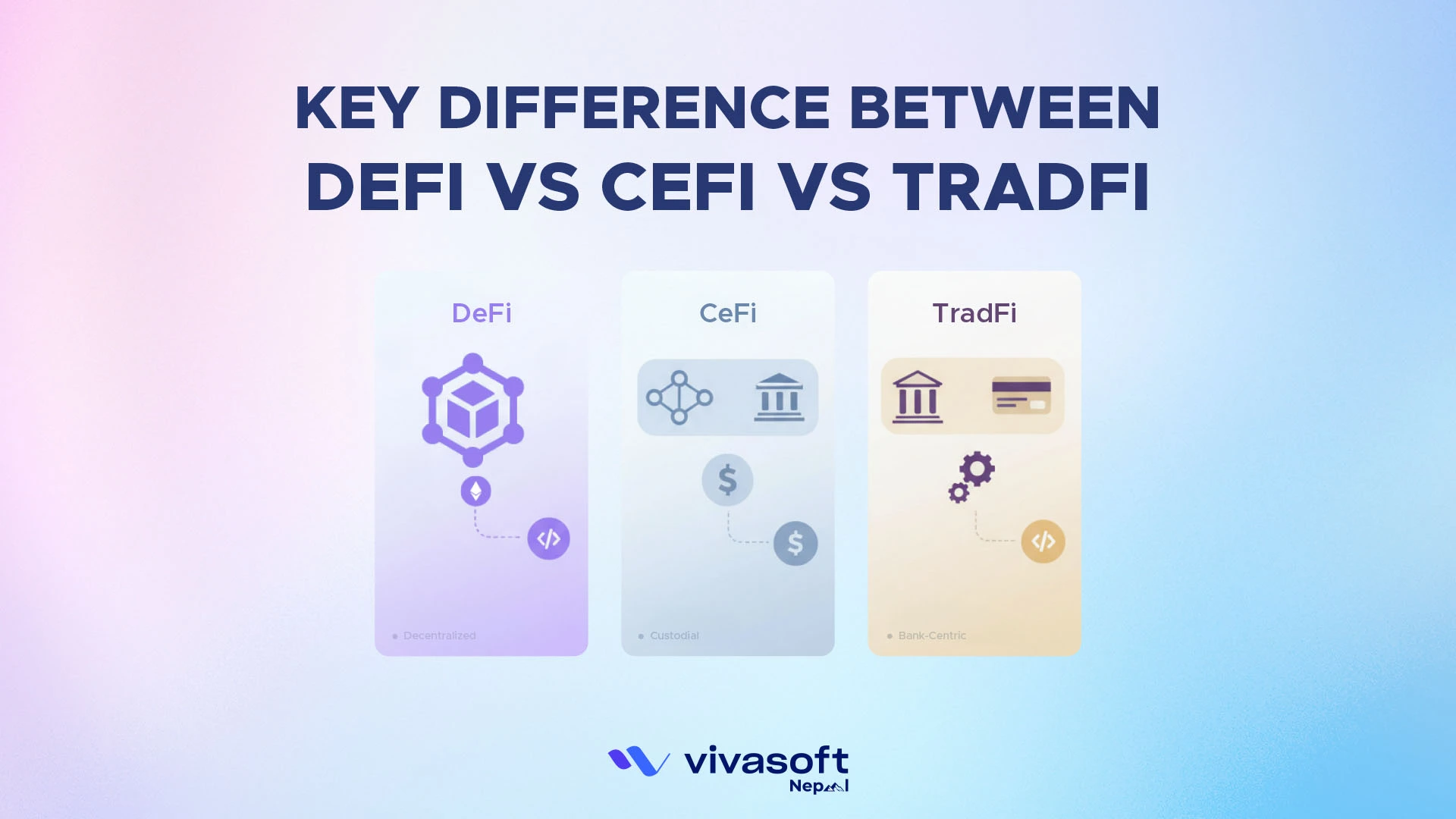

What Is the Key Difference Between TradFi vs CeFi vs DeFi?

Here’s a quick side-by-side look at how these three systems really stack up against each other.

| Feature | TradFi | CeFi | DeFi |

|---|---|---|---|

| Governance | Regulated institutions & central banks | Centralized companies | Code & community (DAOs) |

| Infrastructure | Banks, stock exchanges, payment networks | Company servers & internal ledgers | Public blockchains & smart contracts |

| Primary Assets | Fiat, stocks, bonds | Crypto, stablecoins | Crypto, tokens, stablecoins |

| Custody | Institution holds your funds | Platform holds your crypto | You hold your keys |

| Transparency | Limited, private ledgers | Moderate, internal reporting only | Fully on-chain, public |

| Security | Regulated, insured | Secure but relies on company integrity | Depends on code audits & user vigilance |

| Transaction Speed | Hours to days | Seconds to minutes | Seconds to minutes (blockchain dependent) |

| Costs/Fees | High fees, commissions | Moderate fees, trading & withdrawal charges | Low fees on Layer-2, variable on mainnet |

| Regulation | Strictly regulated by governments | Varies by jurisdiction, some licensed | Minimal regulation, protocol-level governance |

| Liquidity | High for major markets | High on major platforms | Depends on protocol & pool size |

| User Experience | Familiar, traditional interfaces | Easy, app-based | Requires wallet knowledge |

| Accessibility | Limited by geography & KYC | Global but account needed | Permissionless, anyone with wallet can join |

The One Question That Changes Everything: Who Controls Your Money?

It’s simple, who holds the ledger holds the power. TradFi and CeFi put control in people and institutions, DeFi puts it in code and that changes the risks you face.

The Ledger Problem: Banks, Platforms, and Protocols

Here’s the reality: control equal’s risk.

- In TradFi, your bank can freeze your account overnight.

- In CeFi, an exchange can suspend withdrawals without notice.

- In DeFi, a smart contract bug can drain your wallet in minutes.

- The core distinction: TradFi and CeFi rely on people and institutions. DeFi relies on code. Neither is automatically safer; they just expose you to different risks.

Borders, Speed, and the 1.4 Billion Without Banks

International wires can take 3–5 business days and cost $20–$50 in fees. DeFi settles globally in seconds for pennies on networks like Arbitrum.

And for the 1.4 billion adults without bank access (World Bank) , DeFi is permissionless anyone with a smartphone can participate without ID or credit history. Gas fees on Ethereum mainnet can spike to $20–$50 per transaction, making small swaps uneconomical. Layer-2 networks solve this , but most beginner guides skip the details.

Transparency vs. Privacy: Who Can See Your Money?

When it comes to your finances, visibility matters and each system handles it differently.

- TradFi: Your financial data is private to the bank and in some cases, the government.

- CeFi: The platform sees your transactions and balances but this information isn’t public; you’re trusting the company to handle it responsibly.

- DeFi: Wallet activity is fully public on the blockchain though usually not linked to your real world identity. This is a core reason why understanding how decentralized smart contracts operate is important.

The trade-off is clear: TradFi prioritizes privacy, DeFi prioritizes transparency and CeFi sits somewhere in the middle.

Use Cases of TradFi, CeFi and DeFi: How Transactions Actually Differ?

Let’s turn abstract concepts into real world examples so you can see how TradFi, CeFi and DeFi actually work in practice.

Getting a Loan: A Bank vs. an Exchange vs. a Protocol

Loans look very different depending on the system you use.

- TradFi (Bank Loan): Apply, wait 5–15 business days, go through credit checks and income verification. Approval depends on who you are.

- CeFi (Exchange Loan): Deposit crypto on Nexo and get a USD loan in hours. The platform holds your collateral and can liquidate it if prices drop.

- DeFi (Liquidity Pool Loan): Connect MetaMask to Aave, deposit ETH as collateral (150%+), and receive USDC instantly. Smart contracts auto-liquidate if collateral falls no calls, no grace period. This is exactly how modern decentralized lending systems function in practice.

Trading: A Broker vs. an Exchange vs. an AMM

Trading works very differently depending on whether you’re in TradFi, CeFi, or DeFi.

- TradFi (NYSE/Broker): Place a market order during business hours, settle in T+2 and pay brokerage fees.

- CeFi (Binance): Orders execute in milliseconds, settle on the platform’s private database, with zero gas fees and a 0.1% trading fee.

- DeFi (Uniswap): Swap tokens directly against a liquidity pool. Prices are set algorithmically by an AMM and on-chain settlement takes about 12–15 seconds showing how decentralized trading infrastructure operates at scale.

Earning Interest: Savings Account vs. Earn Account vs. Yield Farming

Earning interest works very differently depending on the system you choose.

- TradFi (Savings Account): Deposit funds, earn 0.5%–5% APY with insurance up to $250,000 (FDIC, US).

- CeFi (Coinbase Earn / Nexo): Deposit stablecoins and earn 6%–12% APY. The platform lends your funds to institutional borrowers but your money is at risk if the platform fails.

- DeFi (Compound / Curve Finance): Deposit tokens into a protocol or liquidity pool and earn a variable APY of 5%–25%+. You keep custody but risks include smart contract exploits, impermanent loss and governance failures.

What Is the Risk, Regulation, and Reality of DeFi, CeFi, and TradFi?

Every financial system has its own vulnerabilities. TradFi relies on government oversight and insurance, CeFi depends on the integrity of the company running the platform and DeFi hands trust over to code. By examining historic failures; we can see these risks in action and understand who really bears the consequences when things go wrong.

1. Three Historic Failures: One from Each System

Looking at past failures shows how different risks play out across systems:

- TradFi Failure: Silicon Valley Bank (2023) A bank run wiped $175B in deposits temporarily. Government intervened; most depositors recovered. Lesson: TradFi has a safety net but it depends on political will.

- CeFi Failure: FTX (2022) $8 billion in customer funds vanished due to fraud. No government insurance; users lost everything. Lesson: CeFi depends on company integrity, which isn’t guaranteed.

- DeFi Failure: Terra/Luna (2022) Algorithmic stablecoin collapse erased $40 billion in 72 hours. No company to sue, no regulator, no insurance fund. Lesson: DeFi’s safety net is the code and code can fail catastrophically.

Each system carries risk but the type and source of risk differ dramatically. In TradFi you trust governments and regulations, in CeFi you trust companies, in DeFi you trust code.

Which System Should You Actually Use: TradFi vs CeFi vs DeFi?

Picking the right system comes down to your priorities : how much control you want, the risks you are willing to take and the level of responsibility you are ready for.

Use TradFi If

- You prioritize government-backed deposit insurance.

- You invest in regulated assets like stocks, bonds, ETFs or pensions.

- You need legal protection in case something goes wrong.

- You’re not comfortable managing private keys or crypto wallets.

Use CeFi If

- You want to start with crypto without handling private keys.

- You need a fiat on-ramp; converting bank money to crypto and back.

- You want crypto yields (staking, earn accounts) with some customer support.

- Red flag check: Ensure the platform is licensed, MiCA-compliant (EU) or regulated in your country before depositing.

Use DeFi If

- You understand self-custody and accept responsibility for private keys.

- Your transaction sizes justify gas fees (typically $500+ on Ethereum mainnet; <$10 on Layer-2).

- You want highest yields and are comfortable evaluating smart contract and protocol risks.

- You need 24/7 permissionless access from anywhere without identity verification.

Practical Starting Path for Most Users

For most newcomers, the best way to enter the financial world is step by step start safe, learn gradually and only take on more responsibility once you’re ready.

- Keep emergency savings and traditional investments in TradFi.

- Enter crypto via CeFi platforms like Coinbase or Kraken to learn a market safely.

- Graduate to DeFi once you understand wallets, seed phrases and gas fees; start with funds you can afford to lose entirely.

Frequently Asked Questions

Is defi safer than cefi?

Not necessarily. They just have entirely different risk profiles. CeFi carries heavy counterparty risk (the company steals or mismanages your funds). DeFi carries heavy smart contract risk (a hacker exploits a loophole in the code).

What is the difference between defi and cefi and tradfi?

TradFi is the traditional banking system running on fiat. CeFi is regulated companies giving you access to crypto via a centralized database. DeFi is peer-to-peer crypto finance running entirely on open blockchains without middlemen.

Is xrp considered defi?

Yes, XRP is increasingly considered part of the Decentralized Finance (DeFi) ecosystem, transforming from a bridge asset into a yield-generating token through native Lending Protocol (XLS-66) upgrades and integration with platforms like Doppler Finance and Flare Network.

What does tradfi mean in crypto?

TradFi (Traditional Finance) is the heavily regulated, legacy financial world. In crypto circles, it is used to describe the old way of doing things like trusting a bank with your cash.

How are rwas bridging tradfi and defi?

Real World Assets (RWAs) are taking traditional assets (like real estate or U.S. Treasury bills) and tokenizing them on blockchains. This effectively puts TradFi assets into DeFi liquidity pools.

What are the risks of hacks in cefi vs defi?

CeFi hacks usually target the company’s internal hot wallets or employee credentials. DeFi hacks directly target vulnerabilities in publicly viewable smart contract code.

How to mitigate smart contract risks in DeFi?

If you want to play it safe, stick to “blue-chip” protocols with billions of dollars in Total Value Locked (TVL) that have been publicly battle-tested and audited by multiple tier-one security firms for years. Also, consider buying smart contract insurance protocols.